Macromegas #33 - IPOs, Hypergrowth & Amazon

IPOs, Hypergrowth & Amazon

Hello Friends,

And happy Friday!

There have been 483 IPOs on the US stock market this year, as of May 20, 2021.

That is +718.6% more than the same time in 2020, which had 59 IPOs by this date.

The Single Biggest Determinant of Startup Valuations at IPO 2min

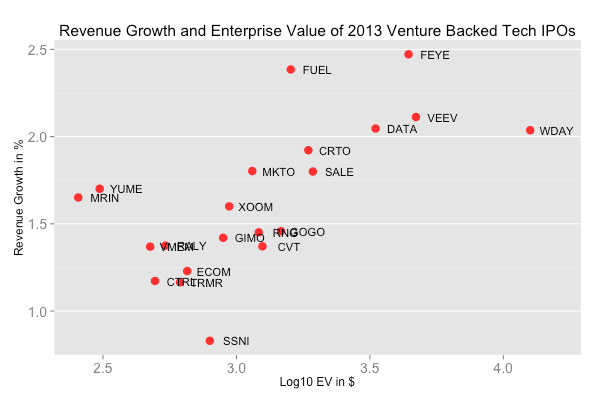

"Growth is king."

The correlation between revenue growth and the enterprise value of the business is 0.51, quite strong.

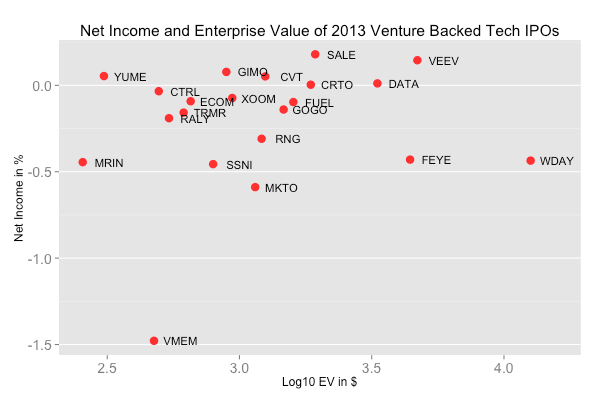

There is no relationship between profitability and the startup’s enterprise value. The correlation between net income and enterprise value is zero.

Amazon Inc. IPOed on the Nasdaq on May 15, 1997, at a price of $18 per share.

Today, a single share is worth ~$3,250, which brings Amazon’s market cap to ~$1.65tn.

That's more than 180,000% growth, i.e. more than 24% CAGR.

Here is a fantastic piece on the eCommerce giant and its strategy, that I curated from a respectable 35min reading time to a bite-sized 10min.

What is Amazon? 35min -> 10min

I am going to answer the question – what is Amazon? – but you can’t begin to understand Amazon without first understanding Walmart. Walmart revolutionized the retail game; Amazon “borrowed” Walmart’s playbook as a starting point, just as Walmart borrowed the playbook from the early discount retailers as a starting point before it.

What is Walmart?

Fundamentally, Walmart’s business was mostly about the first two things that Mr. Walton always mentioned: “a wide assortment of good quality merchandise” at “the lowest possible prices.”

And, for the first four decades or so, Walmart became the best in the world at doing exactly that: using the square footage it had in each store as effectively as possible, stocking it with good quality merchandise at the lowest possible prices, and maintaining sufficient inventory to satisfy the resulting customer demand.

Walmart’s buyers became gatekeepers for access to the largest marketplace on the planet. The buyer’s job was to identify high-quality merchandise that the customer might want, and then negotiate the best possible price.

Sam Walton was the ‘intelligent designer’ behind the Walmart algorithm: that is, a) “a wide assortment of good quality merchandise”, b) offered “at the lowest possible prices,” c) backed by “guaranteed satisfaction” and “friendly, knowledgeable service,” d) available during “convenient hours” with “free parking” and “a pleasant shopping experience,” e) all within the largest, most convenient possible store size and location permitted by local economics.

In other words, the size, layout, format, product mix, and the selection/training of the associates in that Supercenter were the result of the algorithm that Sam Walton had designed.

So, back to our question: what is Walmart? Or, more accurately, what was Walmart, circa 1994?

Walmart can be thought of as a bounded search for the optimal selection, inventory, and pricing of SKUs that a local market could support. It was bound, or constrained, by the characteristics of the local economy

The immensely difficult job of the local management team was to predict and implement the optimal mix that could theoretically have been found if every possible permutation were tested by the local economy.

Enter Amazon

Jeff Bezos had a big realization in 1994: the world of retail had, up until then, been a world where the most important thing was optimizing limited shelf space in service of satisfying the customer – but that world was about to change drastically. The advent of the internet – of online shopping – meant that an online retailer had infinite shelf space. While Amazon did not have the capital to stock every SKU on the planet, nor a warehouse large enough to do so, it didn’t have a constraint on the actual ‘shelves’ themselves.

Bezos, in other words, wanted to build an unbounded Walmart.

In this world of infinite shelf space, it wasn’t the quality of the selection that mattered – it was pure quantity. And with this insight, Amazon did not need to be nearly as good – let alone better – than Walmart at Walmart’s masterful game of vendor and SKU selection. Amazon just needed to be faster at aggregating SKUs – and therefore faster at onboarding vendors.

And so, back in 1994, Amazon kicked off its unbound search for the optimal selection of SKUs. Its algorithm – borrowed and modified from Walmart – was simple: a) a vast selection, b) delivered fast, c) at the lowest possible prices, d) backed by guaranteed satisfaction.

Amazon added as many vendors as it could feasibly add, far outpacing other retailers because of a bar that was far lower. But the pace was too slow; Amazon was aggregating demand – that is, customer traffic – faster than it was aggregating supply – that is, vendor selection. Amazon had bumped up against its first constraint: the speed at which it could add new vendors to its catalog and associated inventory to its warehouses.

In its effort to remove this bottleneck, Amazon had an insight that would dramatically accelerate its strategy of mass SKU-aggregation: what if, instead of the painfully slow process of onboarding and negotiating with vendors, Amazon could instead open its website to third party sellers?

A Cambrian SKU explosion

Amazon Marketplace solved a whole host of problems all at once. By allowing sellers to bypass the gatekeepers altogether, Amazon could rapidly fill its infinite shelf space with a vast selection of SKUs not available from other retailers. And instead of slowly building its own inventory on promising SKUs, Amazon could make a seller’s already-stocked inventory instantly available to eager customers. And, perhaps most importantly, it solved the problem of how to negotiate pricing with a rapidly-expanding SKU base. When Amazon was competing against sellers for a given SKU, there were two possibilities: either Amazon had negotiated the best possible price with the vendor and would ‘win’ the sale, or it had failed to get the best possible price and another seller would win the sale instead – but Amazon would collect a 12-15% commission, and gain a data point that its nascent vendor team could use in price negotiation. And, of course, ‘losing’ the sale to a third party seller still meant that Amazon would keep the customer.

Platforms

To make sense of what started to happen after Amazon rolled out Marketplace, you have to understand that things get really weird when you run an unbounded search at internet-scale. When you remove “normal” constraints imposed by the physical world, the scale can get so massive that all of the normal approaches start to break down.

Walmart had solved problems of vendor management, product management, and bureaucracy at an almost unfathomable scale.

Walmart, at its heart, is a company of merchants; it is a human-powered company, and its advantage in the marketplace is that it merchandises better than any other company on the planet.

Amazon, by contrast, is an illustration of what happens when a massive global market is freed by the internet from the geographical constraints that previously kept it manageable; it is an illustration of what happens when you enter a problem space so large that you have to bypass the human element altogether. What was just barely solvable with carefully-built systems at Walmart’s scale of shelf space would have been impossible to solve with shelf space that stretched on to infinity. Amazon had to find a way of abdicating responsibility for solving these problems altogether; with Marketplace, Amazon had begun to grasp at a solution that would do exactly that.

After removing the vendor bottleneck, Amazon had discovered the next constraint to filling its theoretically-infinite shelf space: computing power and data storage. To his horror, Bezos had discovered that Amazon’s software engineers were waiting weeks for technical resources like servers and storage to be provisioned. Instead of being limited by how fast they could write code, they were limited by how fast they could deploy that code to Amazon’s infrastructure. Amazon began to build a platform that would allow its software engineers to provision on-demand resources immediately. In a radical move, the platform – Amazon’s own technological infrastructure – would be made available to external developers, too. It would be called Amazon Web Services.

Another constraint had emerged around the same time, this time on the customer-facing front: Amazon could no longer practically keep up with the theoretical pace of innovation that its exploding SKU catalog had enabled. In other words, Amazon could not possibly develop features on its website fast enough to take advantage of all the merchandising opportunities that its products had brought.

In a similarly radical move, Bezos decided to expose Amazon’s entire product catalog via an application programming interface – an API – so that any software developer, internal or external, could programmatically access Amazon’s catalog and use the SKU data

And so, circa 2002, we start to see the emergence of a pattern: 1) Amazon had encountered a bottleneck to growth, 2) it had determined that some internal process or resource was the bottleneck, 3) it had realized that it could not possibly develop and deploy enough resources internally to remove that bottleneck, so 4) it instead removed the bottleneck by building an interface to allow the broader market to solve it en masse. This exact pattern was repeated with vendor selection (Amazon Marketplace), technology infrastructure (Amazon Web Services, or AWS), and merchandising (Amazon’s Catalog API).

Captive customers

The problem with having captive customers is that, lacking external competitive pressure, a service inevitably begins to degrade over time. The service provider is removed from the feedback loop, since, 1) given sufficient market power, suppliers can’t feasibly stop using the service, and 2) the service provider itself doesn’t experience the pain of using its own service.

The canonical example here is the DMV: its customers cannot go elsewhere for service, and the DMV does not experience the pain of interacting with itself.

As these examples of the same pattern – Marketplace, AWS, and catalog – emerged around the same time in 2002, Jeff Bezos had the most important insight he would ever have: in the world of infinite shelf space – and platforms to fill them – the limiting reagent for Amazon’s growth would not be its website traffic, or its ability to fulfill orders, or the number of SKUs available to sell; it would be its own bureaucracy. As Walt Kelly put it, “we have met the enemy, and it is us.” In order to thrive at ‘internet scale,’ Amazon would need to open itself up at every facet to outside feedback loops. At all costs, Amazon would have to become just one of many customers for each of its internal services.

And so, as told by former Amazon engineer Steve Yegge, Jeff Bezos issued an edict: 1) All teams will henceforth expose their data and functionality through interfaces, 2) teams must communicate with each other through these interfaces, 3) all interfaces, without exception, must be designed from the ground up to be exposed to developers in the outside world, and 4) anyone who doesn’t do this will be fired.

Platforms, platforms, platforms

Amazon began systematically removing bottlenecks to growth. It found that Marketplace sellers were not particularly adept at shipping directly to Amazon’s customers: Fulfillment By Amazon (FBA) allowed sellers to ship their inventory to Amazon’s fulfillment centers.

Platforms became Amazon’s answer to every growth obstacle it encountered. Platforms became part of the algorithm. Sellers are limited by access to capital? Launch Amazon Lending. Customers can only buy things when they are in front of their computer or phone? Build Echo. UPS and FedEx can only deliver within 24 hours? Launch Amazon Flex and Amazon Logistics.

Amazon assembled a massive machine to deploy its algorithm over and over, and the momentum was unstoppable. Every barrier in its path was solved with a platform – until one of these platforms led Amazon to a catastrophic mistake.

Ads

Amazon Advertising allowed sellers to feature ‘Sponsored Products’ – paid ads that appear at the top of search results. Sponsored Products solved three problems at once: new product discovery for the customers, new product introductions for the sellers, and, as an added bonus, pure gross margin revenue for Amazon – to the tune of $8 billion annually.

The problem with Sponsored Products is that sponsored listings are not actually good for customers – they are good for sellers; more specifically, they are good for sellers who are good at advertising, and bad for everyone else. Paid digital advertising is a very specific skill set; the odds that the brand with the best product also happens to employ the best digital marketing staff or agency is extraordinarily low. Further, the ability to buy the top slot in search results favors products with the highest gross margin – hence the highest bidder – not the products that would best satisfy customers.

Remember that in the world of infinite shelf space, the ranking algorithm is practically the entire merchandising strategy. Organic, customer-centric product rankings – the strategy that brought Amazon to $250 billion in retail revenue – has been permanently distorted.

The platform problem

With infinite shelves that are constantly expanding and filling without constraint, Amazon cannot possibly police the ever-growing universe that it has created.

Bad-actor tactics inevitably surface, and Amazon is in a constant war to keep its own platform consistent with its customer-centric mission. This is a war that Amazon will never be able to “win”; the best it can hope for is to try to keep up with the evolving bad-actor tactics.

Amazon, in other words, has not yet figured out how to extend its internal incentive structure – the incentive structure that has been so successful in keeping the company customer-obsessed – to its external platform participants: the sellers.

So, what is Amazon? It started as an unbound Walmart, an algorithm for running an unbound search for global optima in the world of physical products. It became a platform for adapting that algorithm to any opportunity for customer-centric value creation that it encountered. If it devises a way to keep its incentive structures intact as it exposes itself through its ever-expanding external interfaces, it – or its various split-off subsidiaries – will dominate the economy for a generation. And if not, it’ll be just another company that seemed unstoppable until it wasn’t.

Please don’t forget to share if you think this type of readings can interest others:

Thanks for reading, and have a personal hypergrowth weekend,

V